If you bought, sold, traded, earned, or received cryptocurrency at any point during 2025, the IRS expects you to report it on your 2026 tax return. This isn't optional, and the enforcement infrastructure has expanded significantly.

The direct answer: yes, you must report. Every taxable cryptocurrency transaction must appear on your return, and the IRS now asks a direct question about digital assets on the front page of Form 1040. Checking "No" when you should have checked "Yes" is considered a false statement under penalty of perjury. The IRS has issued John Doe summonses to major exchanges including Coinbase and Kraken, obtained customer records for millions of accounts, and beginning with the 2025 tax year, centralized exchanges must issue the new Form 1099-DA reporting your transactions directly to the IRS. If you held crypto at any point during the tax year, here's exactly what you need to know.

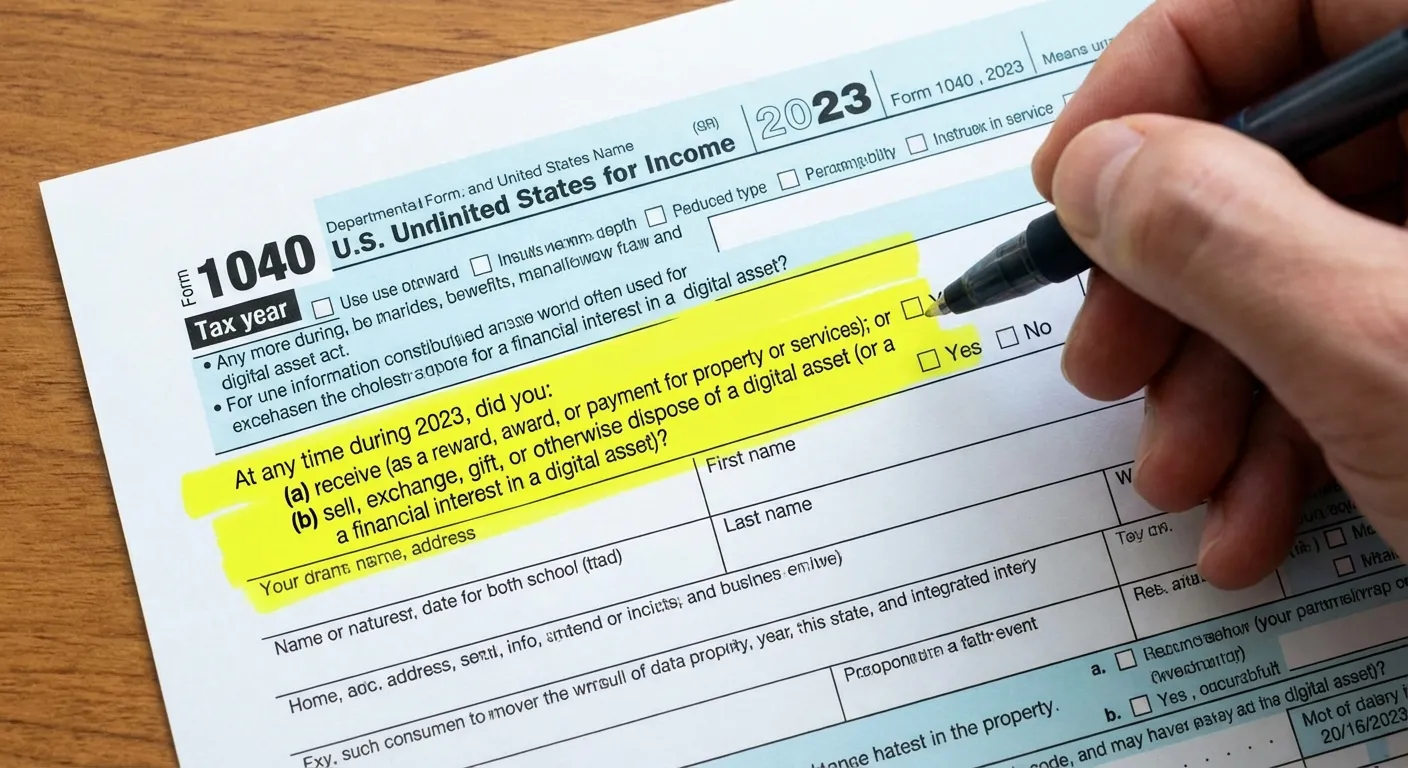

The Form 1040 Digital Asset Question

Since the 2019 tax year, the IRS has included a question about cryptocurrency on Form 1040. The current version asks: "At any time during 2025, did you: (a) receive (as a reward, award, or payment for property or services); or (b) sell, exchange, gift, or otherwise dispose of a digital asset (or a financial interest in a digital asset)?"

You must answer this question regardless of whether you owe any tax. If you simply held cryptocurrency and didn't transact, you can check "No." But if you received staking rewards, sold any amount, traded one cryptocurrency for another, or received crypto as payment for goods or services, the answer is "Yes," even if the transaction resulted in a loss.

The IRS treats this question the same way it treats the foreign bank account question on Schedule B: it's a compliance flag. Answering incorrectly doesn't just risk an audit. It's a false statement on a federal tax return, which carries its own penalties independent of any tax owed.

What Counts as a Taxable Event

Not every interaction with cryptocurrency triggers a tax obligation, but more transactions are taxable than most people realize. Understanding which events create a reporting requirement is the first step to filing correctly.

Capital gains events (reported on Form 8949 and Schedule D): Selling cryptocurrency for U.S. dollars or any fiat currency creates a taxable event. So does trading one cryptocurrency for another, such as converting Bitcoin to Ethereum. Using cryptocurrency to purchase goods or services is also a disposal that triggers capital gains or losses. In each case, you calculate the gain or loss by subtracting your cost basis (what you paid for the crypto, including fees) from the fair market value at the time of the transaction.

Ordinary income events (reported on Schedule 1 or Schedule C): Receiving cryptocurrency as payment for work, whether as an employee or freelancer, is taxable as ordinary income at fair market value on the date you received it. Mining rewards are taxable as ordinary income when you receive them. The IRS clarified in Revenue Ruling 2023-14 that staking rewards are taxable as ordinary income the moment you gain "dominion and control" over the rewards, meaning when you can sell, exchange, or otherwise transfer them. This applies whether you stake directly on a blockchain or through an exchange.

Non-taxable events: Buying cryptocurrency with fiat currency is not taxable. Transferring crypto between your own wallets is not taxable. Donating crypto to a qualified charity is generally not taxable (and may generate a deduction). Receiving a gift of crypto is not taxable until you sell it, at which point you inherit the giver's cost basis.

The New Form 1099-DA and What It Changes

The Infrastructure Investment and Jobs Act, signed in November 2021, expanded the definition of "broker" to include cryptocurrency exchanges and required them to report customer transactions to the IRS. After years of regulatory development, Form 1099-DA (Digital Asset Proceeds from Broker Transactions) takes effect for the 2025 tax year.

Starting with transactions in 2025, centralized exchanges like Coinbase, Kraken, Gemini, and others must report your gross proceeds from cryptocurrency sales and exchanges directly to the IRS, similar to how stock brokerages send Form 1099-B. You should receive your Form 1099-DA from each exchange you used during 2025 by early 2026. For the 2025 tax year, exchanges are required to report gross proceeds but are not yet required to report cost basis. Full cost basis reporting begins with the 2026 tax year.

This is a fundamental shift in crypto tax enforcement. Previously, the IRS relied on voluntary reporting, John Doe summonses, and third-party data matching. Now, exchanges report directly, and the IRS can cross-reference your return against 1099-DA data the same way it matches W-2s and 1099-INTs. If your return doesn't include transactions that appear on a 1099-DA, expect an automated notice. For more on navigating tax forms and free filing options, our guide on how to file taxes free in 2026 covers the available IRS programs.

How to Report: Form 8949 and Schedule D

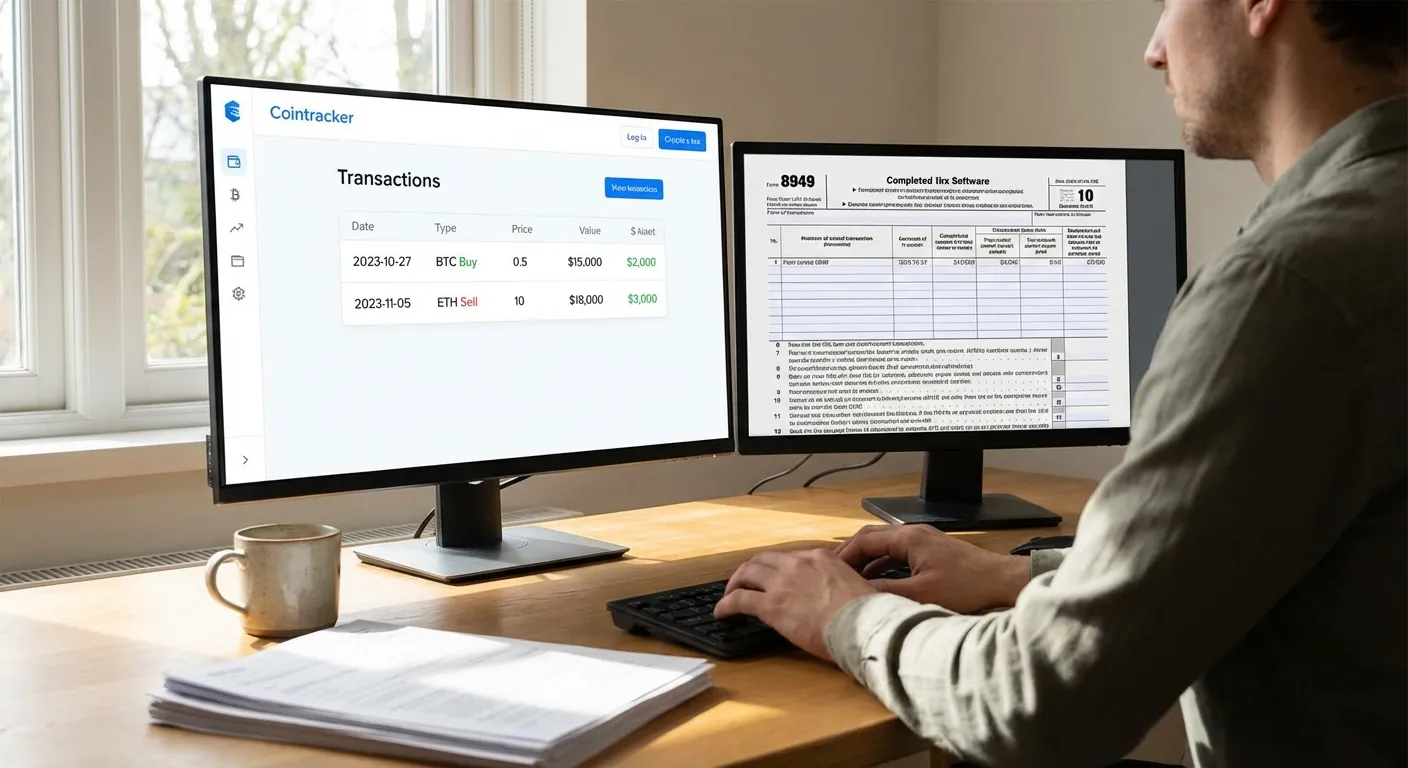

Capital gains and losses from cryptocurrency go on Form 8949 (Sales and Other Dispositions of Capital Assets) and then flow to Schedule D of your 1040. Each transaction gets its own line on Form 8949, which requires the date you acquired the asset, the date you sold or disposed of it, your proceeds, your cost basis, and the resulting gain or loss.

If you had more than a handful of trades during 2025, completing Form 8949 manually is impractical. Crypto tax software tools like CoinTracker, CoinLedger, and Koinly can import your transaction history from exchanges and wallets, calculate your cost basis, and generate a completed Form 8949. These platforms integrate directly with TurboTax, H&R Block, and TaxAct, so you can import the form into your tax filing software.

Short-term vs. long-term rates matter significantly. If you held the cryptocurrency for one year or less before disposing of it, the gain is taxed as short-term capital gain at your ordinary income tax rate (10% to 37% for 2025). If you held it for more than one year, the gain qualifies for long-term capital gains rates: 0% for taxable income up to $48,350 (single) or $96,700 (married filing jointly), 15% for income between those thresholds and $533,400/$600,050, and 20% above that. This difference alone can mean paying nearly half as much tax on the same gain simply by holding for longer than 12 months.

The Cost Basis Trap Most Crypto Holders Fall Into

Starting January 1, 2025, the IRS requires wallet-by-wallet cost basis tracking. Previously, many crypto holders used a "universal wallet" approach, treating all their holdings across exchanges and wallets as a single pool for cost basis calculations. Rev. Proc. 2024-28, issued in July 2024, provided a one-time safe harbor allowing taxpayers to allocate their existing basis across individual wallets before the January 1, 2025 deadline. That deadline has passed, and the allocation is irrevocable.

If you missed this window, your default cost basis method for each wallet is now FIFO (first in, first out), which means the oldest units you hold are treated as being sold first. In a rising market, FIFO tends to produce larger taxable gains because your oldest, lowest-cost units are disposed of first. Specific identification, where you designate exactly which units you're selling, can reduce your tax bill, but it requires meticulous record-keeping and must be documented at the time of the transaction, not retroactively.

This is a common and expensive mistake. Someone who bought Bitcoin at $10,000 in 2020 and again at $60,000 in 2024, then sold some in 2025, would pay significantly different taxes depending on whether FIFO or specific identification applied. If you've been trading across multiple exchanges and wallets without tracking your basis, a crypto tax specialist or CPA familiar with digital assets can help you reconstruct your records before filing. If you're also navigating other new tax provisions this season, our guide on setting up IRS direct deposit for your refund can help you get your money faster once your return is filed.

Penalties for Not Reporting

The consequences for failing to report cryptocurrency transactions range from inconvenient to severe. At minimum, underreporting income triggers a 20% accuracy-related penalty on the additional tax owed. If the IRS determines your failure was willful, civil fraud penalties can reach 75% of the underpayment. In extreme cases involving significant unreported income, criminal tax evasion charges carry up to five years in prison and fines up to $250,000.

The IRS has demonstrated its seriousness about crypto enforcement. It has obtained customer records from Coinbase (approximately 13,000 accounts in 2016), issued John Doe summonses to Kraken for accounts with $20,000 or more in transactions between 2016 and 2020, and expanded its Criminal Investigation division's focus on digital asset cases. With Form 1099-DA now providing automated reporting, the era of flying under the radar with crypto gains is effectively over.

Key Takeaways

Yes, you must report cryptocurrency on your 2026 tax return if you sold, traded, earned, or received crypto during 2025. The Form 1040 digital asset question requires a truthful answer. Use Form 8949 and Schedule D for capital gains, and report ordinary income (mining, staking, payments) on the appropriate schedules. The new Form 1099-DA means exchanges are reporting your transactions directly to the IRS. If you have complex holdings across multiple wallets, consider crypto tax software or a qualified tax professional to ensure accurate cost basis tracking. Failing to report isn't worth the risk: the IRS has the data, the tools, and the enforcement appetite to follow up.

This article is for informational purposes only and does not constitute tax advice. Consult a qualified tax professional for guidance specific to your situation.

Sources

- Your Cryptocurrency Tax Guide - TurboTax

- Digital Assets - Internal Revenue Service

- Rev. Proc. 2024-28: Crypto Cost Basis Rules - CoinLedger

- IRS Guidance on Staking Rewards (Revenue Ruling 2023-14) - BDO

- Crypto Taxes Guide: 2025-2026 Rates and Rules - NerdWallet